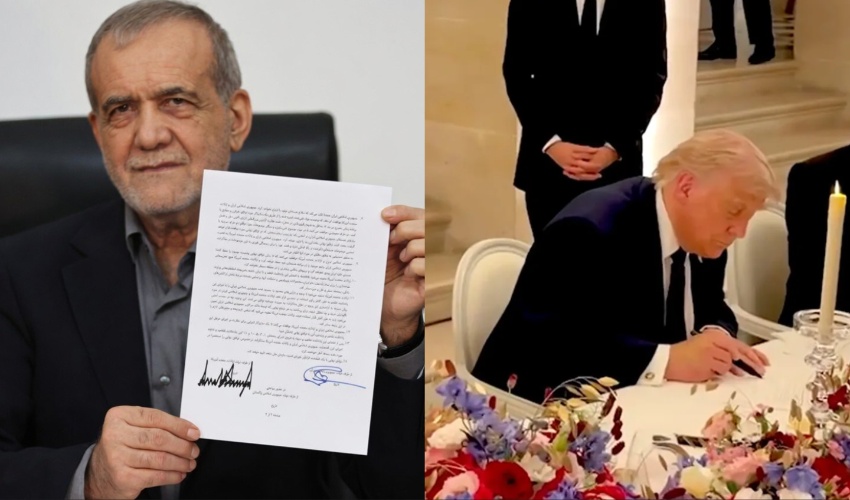

Iran is set to receive broad financial incentives under its proposed agreement with the United States, including immediate permission to sell oil, access to a $300 billion development fund and eventual release of frozen assets, according to a final draft reported by Bloomberg News.

The draft memorandum of understanding provides the clearest picture yet of the economic benefits Iran could receive in exchange for ending its chokehold on the Strait of Hormuz and reaffirming its commitment never to seek a nuclear weapon.

The two sides agreed to the framework on Sunday and are expected to formally sign it on June 19 in Switzerland. The signing would open the way for 60 days of negotiations aimed at ending the war permanently and placing strict new limits on Iran’s nuclear programme.

Neither Washington nor Tehran has formally released the text of the agreement. However, Bloomberg reported that the United States has started circulating the document with allied nations at the G7 summit in France.

A person familiar with the matter said technical details were still being finalized, meaning the precise wording may change before the signing ceremony.

US officials have also given different timelines for when the agreement will be made public. President Donald Trump has said the text will be released sometime after Friday’s signing ceremony, while a senior US official said Monday that it could be published within days.

Signing planned at Swiss resort

According to the Swiss foreign ministry, the ceremony is scheduled to take place at the Bürgenstock, a mountain resort overlooking Lake Lucerne.

Vice President JD Vance is expected to lead the American delegation, while Iran is likely to be represented by Parliament Speaker Mohammad Bagher Ghalibaf.

US to issue immediate oil waivers

Under the terms of the draft, the US Treasury Department “will issue waivers for exports of Iranian crude oil, petrochemical products and their derivatives” immediately after the memorandum is signed.

The United States will also end its naval blockade of Iran. Both countries will work to ensure that traffic through the Strait of Hormuz returns to prewar levels within 30 days.

A senior US official said the agreement allows Iran to immediately begin selling oil and fuel, including banking, transportation and insurance services needed to facilitate those sales.

However, another person familiar with the matter said the US understanding is that the oil sales apply only to Iranian oil already loaded onto tankers, not a broader authorization for Iran to fully resume exports.

Strait of Hormuz to reopen

The memorandum extends a fragile ceasefire announced in April for another 60 days. During this period, the two countries will negotiate a permanent truce.

Under the deal, the US will end its blockade of Iranian ports, while Tehran will restore the passage of oil tankers and other maritime traffic through the Strait of Hormuz.

The strait, which normally carries around one-fifth of the world’s oil and liquefied natural gas trade, has been effectively blocked since the US and Israel launched strikes on Iran on February 28.

Both sides say the Strait of Hormuz will reopen from Friday. However, shipping companies have signaled caution and are waiting to see whether the peace process holds.

Iranian state television reported on Tuesday that operations to lift the maritime blockade had begun, while stressing that vessels must still coordinate with Iran’s Revolutionary Guards.

The US has said the strait will remain open toll-free for 60 days and expects that arrangement to be included in the final agreement. Iran has suggested it will retain control over the strait along with Oman.

$300bn development fund planned

According to the draft document, the US and its regional partners would prepare a plan to rehabilitate Iran and support its economic development with financing of at least $300 billion.

Trump earlier denied that the US would pay Iran $300 billion. The draft states only that the US and its partners would ensure financing of that amount.

US and Iranian officials say the deal could eventually provide major economic benefits to Iran through sanctions relief, the release of frozen assets and the creation of a $300 billion reconstruction fund.

The fund is expected to be financed by neighbouring Gulf states that host US military bases and were hit by Iranian attacks during the war, provided Iran complies with the terms of the deal.

Frozen assets and sanctions timeline

The draft is vague on the release of Iran’s frozen assets, saying the US undertakes that those funds “will be released and made fully available,” but without giving a clear timeline.

Iran has been under US sanctions since the 1979 revolution that overthrew the shah. According to an Atlantic Council analysis, around $12 billion in Iranian funds were frozen at that time.

Over the following decades, Iran faced additional US and international sanctions, especially before the 2015 Joint Comprehensive Plan of Action, also known as the JCPOA.

The draft says the US would commit to ending sanctions against Iran, but only as part of a final agreement to be negotiated over the next two months.

Washington would also begin withdrawing its military forces “from the surrounding areas” within 30 days of a final agreement.

Status quo to remain during talks

According to Bloomberg, both countries have agreed to maintain the status quo until a final agreement is reached.

Iran will maintain its current nuclear programme, while the United States will not impose new sanctions or increase its military presence during the 60-day negotiation period.

The goal is to reach a final agreement within a maximum of 60 days, though the timeline may be extended if necessary.

During this period, both sides will be required to refrain from any aggressive action or threats.

Nuclear issue left for final deal

The draft does not directly address the current state of Iran’s enriched uranium stockpile. It only states that the fate of Iran’s enriched uranium “will be adequately addressed in a final agreement,” along with other nuclear issues.

Iran has again reiterated its commitment that it will never develop nuclear weapons. Tehran has long maintained that its nuclear programme is peaceful and that it does not seek an atomic bomb.

Trump described the agreement as a “wall to a nuclear weapon” for Iran and said it clearly states that Tehran will not have a nuclear weapon.

The US president said Iran’s leaders “have to prove themselves” before any broader investment or deeper engagement takes place.

Trump calls deal ‘done deal’

Speaking at the G7 summit in France, Trump said the agreement was a “done deal” that would prevent Iran from developing nuclear weapons. He added that the United States would not pay war reparations or invest money in Iran.

Trump said he liked the idea of sending the Iran agreement to lawmakers in Congress for review after some Republicans complained they were being left in the dark.

The president has also faced criticism from lawmakers for launching the war without congressional authorization, a conflict that remains broadly unpopular among Americans.

Deal faces criticism in US

The agreement carries political risks for Trump, who for years criticized the 2015 Iran nuclear accord signed under former president Barack Obama, calling it a major financial giveaway to Tehran.

Trump withdrew the United States from that agreement in 2018 and promised a stronger deal.

Now, as he moves to wind down the conflict launched by the US and Israel on February 28, some Republican allies and Iran hawks outside the administration are warning that the deal may give Tehran too many financial benefits without enough concessions.

Israel, Lebanon remain key challenges

Another major challenge is the draft’s language stating that the war will end “on all fronts, including in Lebanon.”

That would require consent from Israeli Prime Minister Benjamin Netanyahu, who has so far refused to end Israel’s war against Hezbollah across Israel’s northern border.

Israel has not directly participated in the negotiations and has distanced itself from both the April ceasefire and the latest US-Iran agreement.

Netanyahu said on Monday that Israel is not bound by the agreement and will not withdraw from southern Lebanon.

Vice President JD Vance, however, said the agreement includes Israel and Lebanon, contradicting Netanyahu’s position.

A Hezbollah spokesperson told Reuters that the group believed Iran would not agree to a permanent truce unless Israeli occupation was ended.

Iran’s military command, Khatam al-Anbiya Central Headquarters, warned that Israel should expect a hard response if it does not stop attacks on southern Lebanon.

The war has affected most countries in the region, killing more than 7,000 people, mostly in Iran and Lebanon. Israel invaded Lebanon in March after Iran-allied Hezbollah joined the fighting.

Trump has publicly criticized Netanyahu and expressed frustration with Israel’s military campaign. Speaking on Tuesday, he said he was “not happy” with the way Israel had handled itself.

Difficult negotiations ahead

During the next 60 days, negotiators are expected to address difficult issues, including the future of Iran’s nuclear programme, enriched nuclear material and other sensitive matters.

Iran had been discussing its nuclear programme with Trump administration officials in February before the talks were interrupted by the US decision to launch the war.

Two issues that Trump and Netanyahu cited to justify the war do not appear to be on the immediate agenda: ending Iran’s support for regional armed groups and curbing its missile programme.

Trump said Iran wants to move forward with the process, adding that Tehran “has to get back to business” and that the relationship is now “normalized.”

Oil prices fall after agreement reports

Oil prices have fallen sharply since Trump said late last week that an agreement was imminent.

Brent crude traded below $80 a barrel after sinking 15% over four days, its longest losing streak this year, as markets bet that reopening the Strait of Hormuz would bring a major wave of supply.

On Tuesday, oil prices slid more than 2% to new three-month lows, a day after dropping nearly 5% following news of the deal.

However, industry officials warned that Middle East oil and gas output could take months to fully recover.

.jpg)